PCCA Cotton Market Weekly

July 6, 2026

The Week Ahead

- Cotton enters a relatively quiet week, with Friday’s USDA WASDE supply and demand report expected to receive most of the attention.

- Friday’s report will focus on incorporating last week’s acreage data and updating global supply-and-demand estimates, with USDA now working from the higher cotton acreage number released last week.

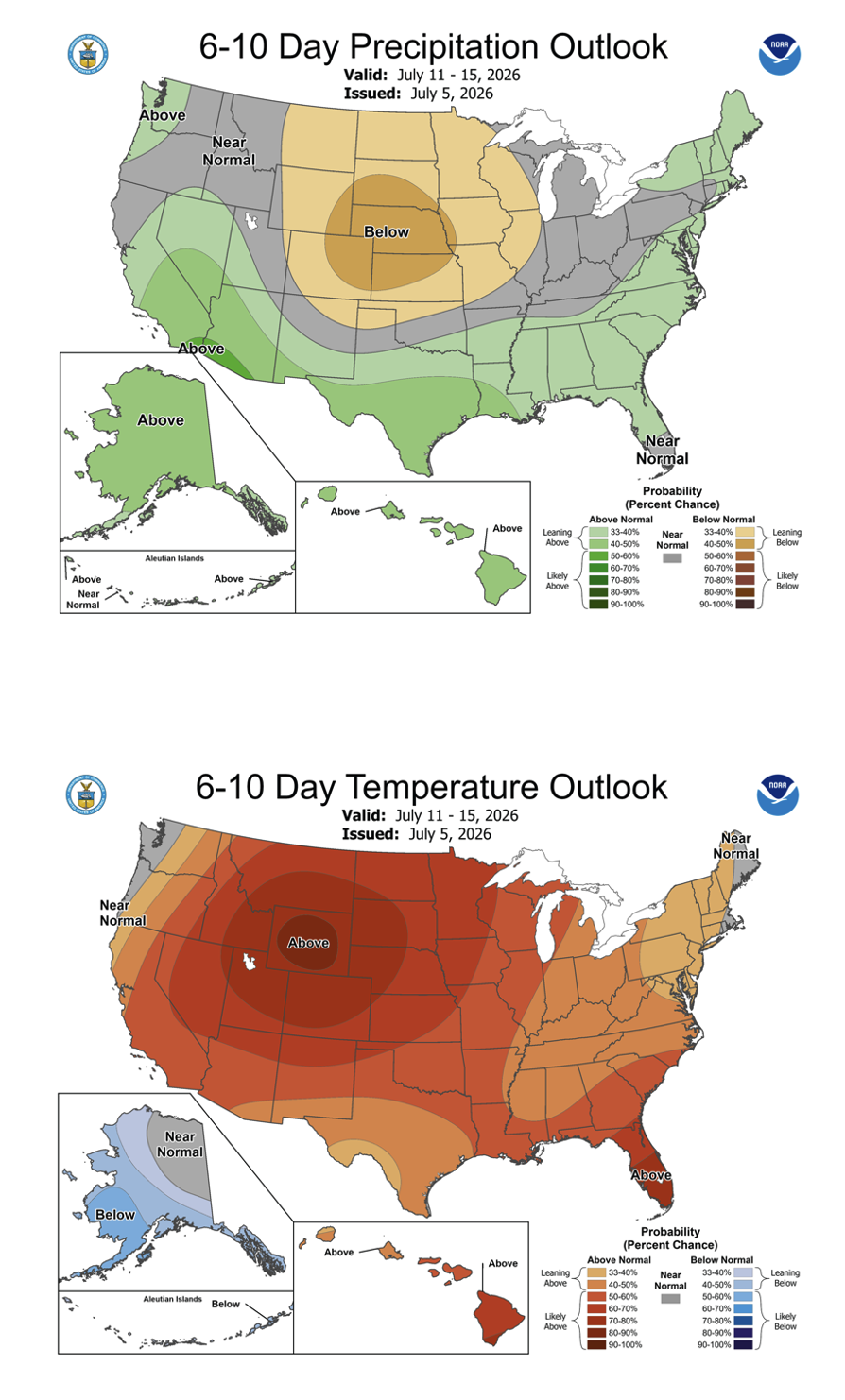

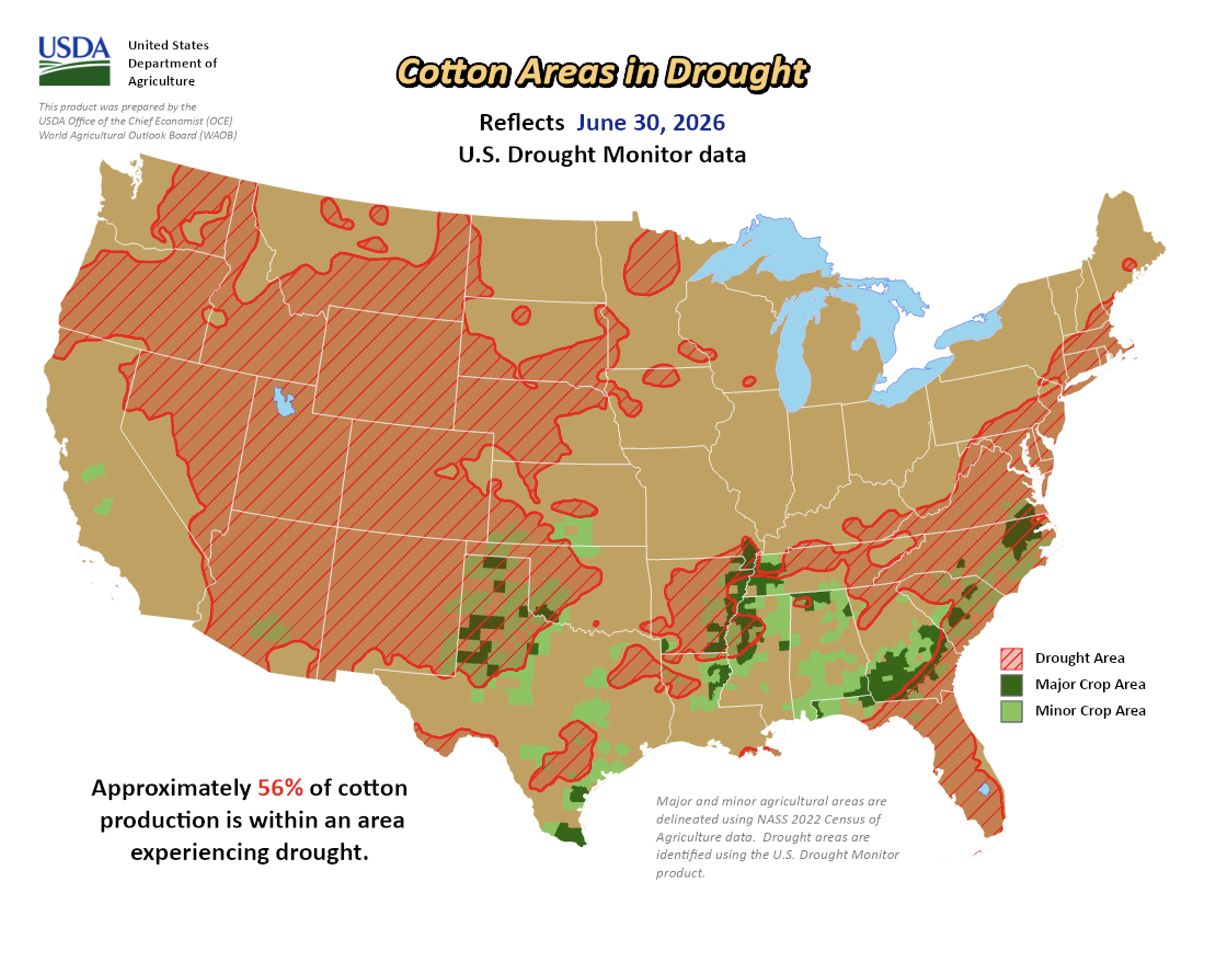

- Weather is one of the market’s biggest drivers. Forecasts favor much of the Cotton Belt, limiting weather-related risk. Even with beneficial rainfall this past week, West Texas could still use additional moisture after spotty showers, while parts of South Texas would benefit from a stretch of drier weather. As weather concerns fade and crude oil plays a smaller role in the market, cotton may struggle to build meaningful upside momentum in the near term.

- The macro calendar is relatively light this week. Markets will watch Wednesday’s release of the Federal Reserve’s meeting minutes for additional insight into the central bank’s outlook on inflation and interest rates, while attention is already shifting toward next week’s CPI report.

- By the end of the week, the market should have a clearer picture after Monday’s delayed CFTC Commitments of Traders report, Thursday’s Export Sales Report, and Friday’s USDA WASDE report. Together, they will provide fresh insight into speculative positioning, export demand, and the overall supply and demand outlook for the new crop.

Market Recap

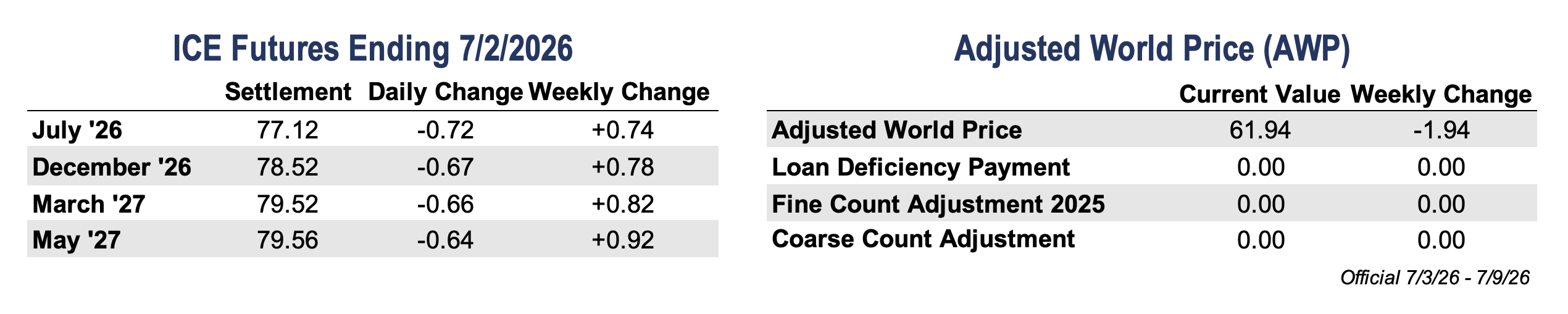

- Cotton futures closed the holiday-shortened week slightly higher, but it wasn’t because of any one major catalyst. The market spent the week digesting a slightly larger-than-expected U.S. cotton acreage estimate, disappointing export sales, and a weaker-than-expected jobs report. Unlike recent weeks, crude oil wasn’t the main story, as prices traded in a relatively narrow range and had little impact on cotton.

- December futures settled at 77.12 cents per pound on Thursday, gaining 74 points over the four trading days.

- USDA estimated U.S. cotton planted acreage at 9.85 million acres, 210,000 acres above the March survey and 567,000 acres above 2025 acreage. While that added to expectations for a larger crop, the report was close enough to pre-report estimates that the market quickly shifted its attention elsewhere.

Economic and Policy Outlook

- June’s Employment Report fell well short of expectations, with the U.S. economy adding just 57,000 jobs versus expectations of 113,000 after downward revisions to the previous two months. The unemployment rate fell to 4.2%, though the decline reflected lower labor force participation rather than stronger hiring. The weaker report increased expectations for Federal Reserve rate cuts later this year and pressured the U.S. dollar. While a weaker dollar is generally supportive for U.S. exports and commodity prices, cotton futures failed to follow that broader macro signal.

- USDA announced $500 million to expand domestic fertilizer production, citing higher input costs following disruptions tied to the Iran conflict and the Strait of Hormuz. The funding will support expansion of existing fertilizer plants and construction of new facilities, though additional production is unlikely to reach the market before the 2027 or 2028 crop years. The announcement complements recent trade actions aimed at lowering fertilizer costs in the near term while increasing U.S. production capacity over the longer term. USDA has not yet released application details or eligibility requirements for the program.

- OPEC+ approved another production increase for August as oil exports through the Strait of Hormuz recover. With geopolitical concerns easing and additional supply expected to enter the market, crude oil prices are under downward pressure. Crude is no longer the primary driver of cotton prices, though lower energy prices remove another source of outside market support.

Supply and Demand Overview

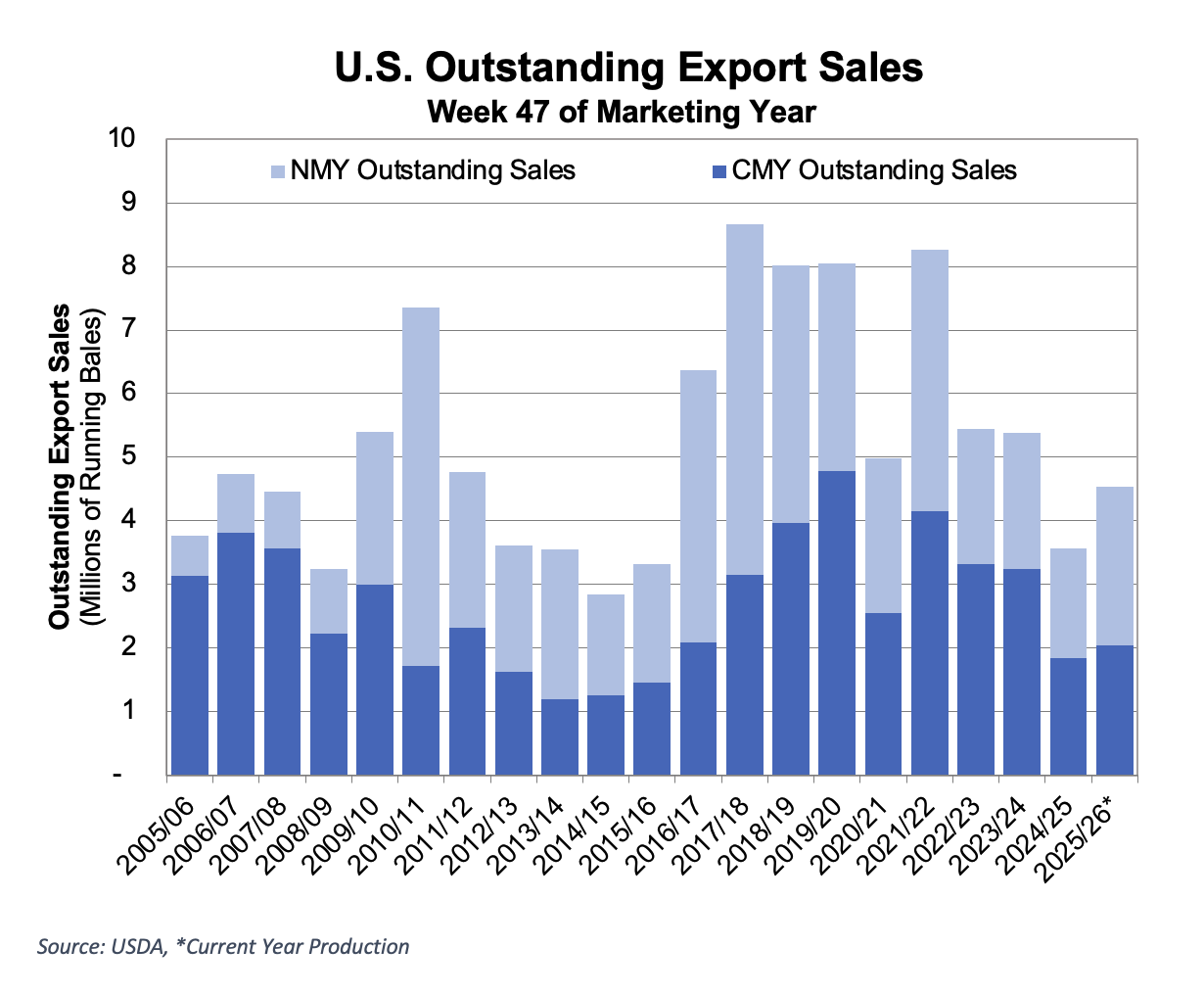

- Overall, this week’s Export Sales Report leaned bearish, with both sales and exports slowing from the previous week. Upland sales totaled just 49,000 bales for the current marketing year, down 42% from the previous week and 70% below the four-week average. Vietnam, India, and Pakistan led buying activity. New crop sales totaled 44,100 bales, led by Honduras, Guatemala, Turkey, Mexico, and Peru.

- Exports reached 218,800 bales, down 27% from the previous week and 22% below the four-week average. Shipments are running at a pace consistent with USDA’s 12.2 million bale export forecast through the final weeks of the marketing year. Although demand has slowed, cumulative export commitments provide underlying support as the marketing year winds down.

- Pima sales fell to a marketing-year low of 700 bales, while exports climbed to a marketing-year high of 24,400 bales.

The Seam®

- As of Thursday afternoon, grower offers totaled 1,164 bales. The past week 12 bales traded on the G2B platform received an average price of 25.00 cents per pound. The average loan redemption rate (LRR) was 6.05, bringing the average premium over the LRR to 18.95 cents per pound.

- Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).